This article is written by Nomentia

Summary. A payment hub solution is a key technology to centralized cash management. Fragmented payment systems, manual payment processes, and the lack of real-time cash flow visibility pose significant challenges that can quickly lead to inefficiencies and risk management issues. In this article, based on our chat with treasury expert Pia Charron, we’re answering questions on how to implement a payment hub and what the best practices are payment hub implementation.

We cover what a payment hub is in detail in this article, top 9 best payment hub solutions in 2024 here, and how to choose a payment hub solution here.

As the financial landscape evolves ever more rapidly, many finance professionals are looking to implement a payment hub to streamline cash management processes and payment operations. To delve deeper into this topic, I had the privilege of interviewing Pia Charron, a lead consultant at Nomentia with over two decades of experience in treasury and cash management systems.

With her extensive expertise, Pia provided invaluable insights into the intricacies of payment hub implementation and the key factors driving its success.

Meet Pia Charron: A treasury expert

Pia’s journey in the realm of treasury began over 20 years ago and with an extensive experience like that, there’s precious little she doesn’t know about implementing cash management and payment management systems.

At Nomentia, she plays a pivotal role as a lead consultant, guiding clients through their cash management projects. Whether it is working with large multinational corporations or SMEs, Pia’s expertise spans various sectors, offering tailored solutions to meet each client’s unique needs.

Today’s finance professionals face increasing challenges from fragmented payment systems, manual processes, and lack of real-time visibility into cash flows. It’s well known that this can result in inefficiencies, errors, and difficulties in managing liquidity and risk effectively. As things stand, it’s no wonder that forward-looking finance professionals are considering implementing a payment hub that can centralize payment operations, automate manual tasks, and gain real-time visibility into financial transactions.

“Payment hubs are piece of key technology to built a risk-aware, efficient and accurate controls in payment operations.”

During our chat, Pia emphasized the critical role these hubs play in enhancing efficiency and accuracy within cash management systems. By centralizing payment operations, businesses are able to significantly reduce errors and manual work while gaining better control over their financial processes. But success in payment hub implementation, as in so many other things, depends on having a clear understanding of what customers want and what they need.

At the heart of payment hub implementation is the need for organizations to consolidate their payment operations. Instead of dealing with multiple banking platforms and disparate systems, a payment hub integrates all payment activities into a single, cohesive system. Central to any successful payment hub implementation is understanding how these diverse customer needs are recognized and fulfilled. Pia highlighted two primary categories of customer requirements: those seeking centralization and efficiency, and those aiming for visibility and control over their payment ecosystems. Whether it’s a multinational corporation or an SME, the customer’s goals dictate the approach to payment hub implementation.

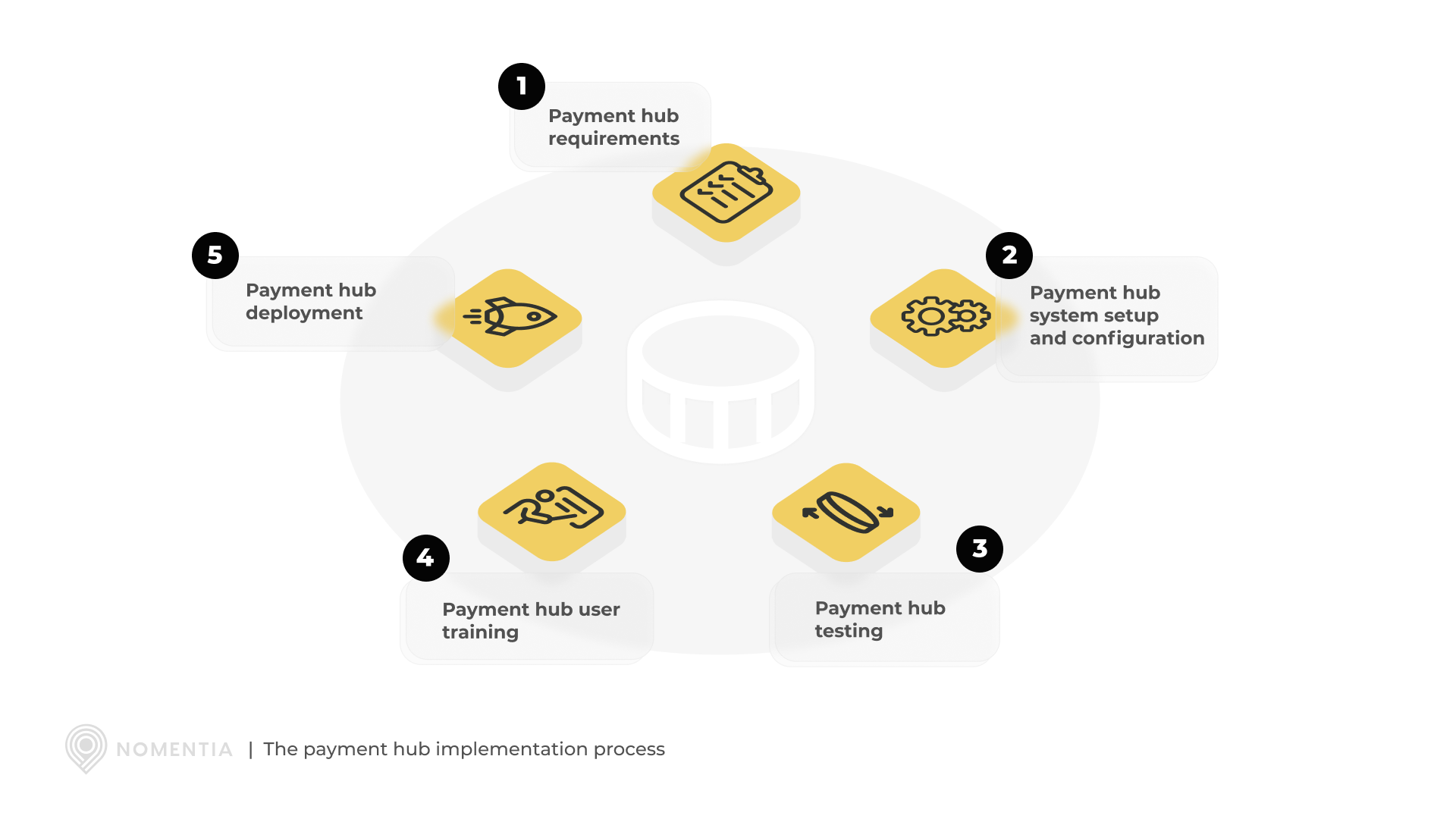

Although each business has its own goals and requirements, all payment hub implementations start with the same situation; with an understanding of three key things: First, what goals the customer has for their payment operations; second, analyzing their current payment ecosystem and processes; and finally, collaborating to devise a strategy on how the customer’s goals can be achieved through the implementation of a payment hub:

To get your payment hub up and running, you have to start by defining the specific requirements for the payment hub implementation, including master data, required bank connections, necessary user roles, and security controls.

Once the scope of your payment hub is settled, next up is setting up and configuring your payment hub system based on defined requirements.

Before being deployed, your newly set up payment hub requires rigorous testing to ensure the system functions as intended and meets requirements.

The key component to effective payment hub implementation is training the admin users who can best communicate and engage internal stakeholders and train payment hub end-users on how to use it effectively.

Once the testing of your new centralized payment hub is done and users are trained, it’s time to go live.

Navigating through the implementation process of a payment hub requires a systematic approach. Pia outlined the various steps involved, starting from defining customer requirements to system setup, testing, training, and deployment. Each stage is important and should be meticulously planned and executed in collaboration to ensure payment hub implementation success.

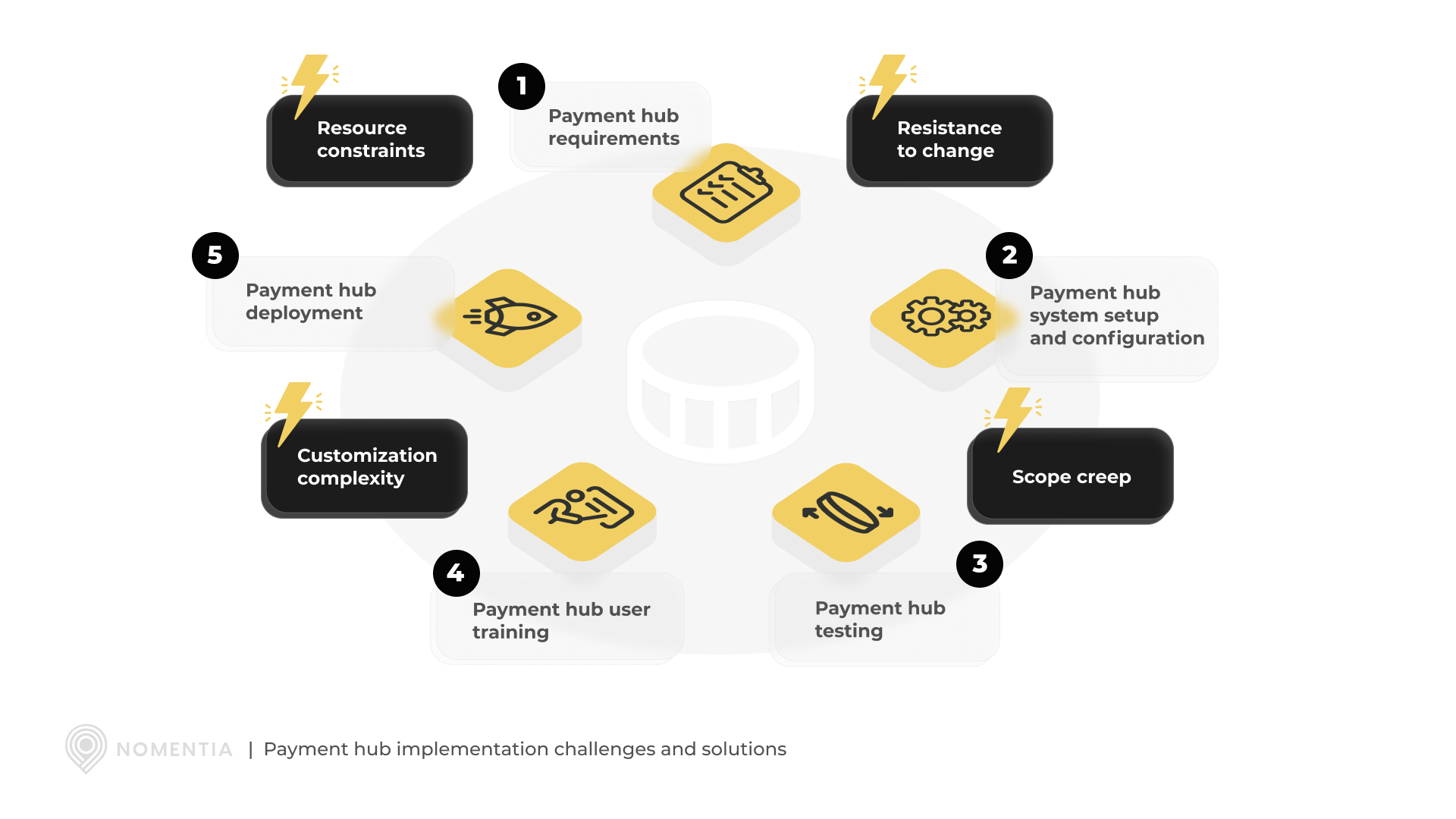

Despite the benefits, payment hub implementation comes with its own set of challenges. As Pia emphasized during our interview, these challenges often stem from the complexity of integrating the payment hub with existing systems and processes, which can require meticulous planning and coordination. Other common payment hub implementation challenges include:

Change can be scary so, it’s not entirely unheard of that employees may resist adopting new processes and technologies, which can lead to implementation delays.

Once initial plans for payment hub implementation are made, the project scope may expand beyond the initial plans. This can, if not carefully managed, lead to additional costs and increased timelines.

As the payment hub is an important system that needs to support business payment operations comprehensively, customizing or tailoring the payment hub to meet specific business needs often comes up. It’s vital to be mindful of the fact that these emergent needs can be complex and time-consuming, while not serving the initially defined goals of the payment hub implementation project.

The limited availability of skilled resources, both internally and externally, can hamper the payment hub implementation process and lead to delays or suboptimal outcomes. It is always wise to be aware of possible pitfalls in payment hub implementation, as they can be avoided and addressed with the support of an experienced partner through:

Comprehensive planning to identify potential integration challenges helps in developing strategies to mitigate them.

Implementing effective change management strategies, including communication, training, and stakeholder engagement, encourages adoption, while regularly reviewing and managing the project scope helps to prevent scope creep and helps the project stay within budget and timeline constraints.

Conducting thorough testing at each stage of your payment hub implementation to identify and resolve technical issues proactively allows the implementation to stay on track.

Assigning the right roles and responsibilities ensures that the payment hub implementation process runs smoothly and efficiently, with clear accountability and direction at every stage. Each role is essential in addressing specific challenges and tasks, ensuring that data migration, regulatory compliance, vendor management, and resource management are effectively handled. This organized approach maximizes the likelihood of successful implementation, minimizes risks, and ultimately leads to the achievement of the organization’s payment processing goals.

Choosing a reliable vendor with a proven track record of support and maintenance ensures your payment hub’s success beyond implementation.

“Success in payment hub implementation requires clear vision and expectation management.”

Pia’s sentiments emphasized the importance of having a clear vision and managing expectations throughout the process. Time and expectation management are critical, and consultants like Pia play a crucial role in addressing these challenges and ensuring project success.

Unlocking the full potential of payment hub implementation requires a deep understanding of industry standards, technical prowess, and collaborative engagement with seasoned professionals. As Pia highlighted: The value of an experienced payment hub provider lies in their comprehensive grasp of not only the pain points faced by finance and treasury professionals during payment hub implementation but also the technical intricacies of payment hub technology. Moreover, it’s crucial for them to possess the ability to listen attentively and comprehend not just the customer’s needs but also the most efficient way to assist them in achieving their objectives.

“Precise, accurate and controlled payment processes sit at the heart of strategic cash and treasury management.”

Cash management and treasury management are indispensable functions that underpin strategy, sustainability, and liquidity. Within this framework, the payment hub emerges as a vital technology. While seasoned finance and treasury professionals typically have a clear vision of their requirements, they greatly benefit from collaborating with experienced counterparts on the vendor side. These cash and treasury technology experts can offer insights gleaned from not only a few but hundreds and thousands of implementation projects that are all business-critical. This depth of experience and expertise is essential for navigating industry standards and anticipating future developments. Hence, when seeking guidance on best practices in payment hub implementation, Nomentia consultants draw from their wealth of experience to offer recommendations that consistently garner the trust and acclaim of our customers, as evidenced by our customer reviews.

Payment hub implementation is a critical aspect of modernizing your cash management strategies. With insights from experts like Pia Charron covered here, businesses can navigate through the complexities of payment hub implementation with confidence. By understanding their needs, following a systematic approach, and fostering collaboration, businesses can achieve success in their payment hub projects, paving the way for enhanced efficiency and control in their financial operations.

A payment hub serves as the central nervous system of financial transactions, orchestrating payments seamlessly across various channels and platforms. Check out these six steps to payment hub implementation success (slideshow):

The complexities of payment hub implementation can seem daunting, but they are by no means impossible to manage. While there are challenges to be faced and critical factors to consider payment hub implementation projects can be successfully navigated if approached with a willingness to learn from the process. You don’t have to reinvent the wheel, just pay heed to what you can learn from others.

1. What are the key challenges organizations face when implementing a payment hub?

Organizations often encounter challenges related to integrating the payment hub with existing systems, such as complex network setups and manual processes. Negotiating varying protocols, interfaces, and connections with banks adds another layer of complexity. A clear understanding of the payment processes post-implementation and how the payment hub addresses pain points can mitigate risks. To tackle the challenges of payment hub implementation, we recommend this article about implementing a global payment hub.

2. What are the critical factors for successful payment hub implementation?

Successful implementation requires meticulous planning, effective stakeholder engagement, and comprehensive training. It’s essential to establish clear objectives, prioritize requirements, and select the right vendor or solution. Collaboration with experienced professionals helps navigate challenges and ensure a smooth transition. Additionally, robust testing procedures and ongoing support are vital for post-implementation success.

3. What are the key stakeholders in the payment hub implementation process?

Stakeholders, including finance, IT, procurement, and executive leadership, play a crucial role in driving the implementation process. Effective communication of project goals and objectives, along with gaining buy-in and support from stakeholders, is essential. Establishing a cross-functional project team ensures alignment of goals and requirements, leading to project success.

Extra: What’s the key to a successful payment hub implementation?

Experienced experts provide invaluable support by leveraging their extensive knowledge of industry standards and hands-on experience with payment hub implementations. They offer guidance on best practices, help identify potential challenges, and provide tailored solutions to meet the organization’s needs. Their expertise fosters collaboration, minimizes risks, and ultimately leads to successful implementation and improved efficiency. To learn more about Nomentia’s expertise, get in touch here.

As the financial landscape evolves, finance professionals are turning to payment hubs to streamline cash management and payment operations. Fragmented payment systems, manual processes, and lack of real-time cash flow visibility pose significant challenges, leading to inefficiencies and risk management issues. To reach their goals, forward-thinking finance experts are implementing payment hubs to centralize operations, automate tasks, and achieve real-time transaction visibility.

Treasury Mastermind is a community of professionals working in treasury management or those interested in learning more about various topics related to treasury management, including cash management, foreign exchange management, and payments. To register and connect with Treasury professionals, click [HERE] or fill out the form below to get more information